The Covid slump of 2020-21 was basically a supply-side shock due to the global spread of the Covid-19 virus and the failure of governments in the major economies (with a few exceptions) to prevent its spread. There were delayed and bungled measures along with weakened health systems, so economies had to close down as lockdowns and isolation measures were the only answer to avoiding catastrophe. Economically, that meant supply stopped, and then that led to a collapse in demand as people were laid off and businesses crashed.

But recovery is now under way (more or less) in most major economies. Demand was propped up in the major advanced economies through massive government fiscal spending and central bank injections of credit for businesses (particularly large ones). And now through a combination of lockdowns and the incredibly fast development and rollout of effective vaccinations (thanks to publicly funded science), the major economies are now able to recover.

But in the G7 economies this initial recovery has the aspect of a “sugar rush.” The “sugar” of fiscal stimulus and historic levels of easy credit is infusing capitalist businesses and household spending with an energy boost.

Indeed, during the pandemic slump sections of capitalism did not suffer at all; on the contrary, they gained hugely, e.g., the social media and tech sector, the mega-distribution companies, and Big Pharma.

Better-off households also suffered less (at least materially) as they continued to be paid, could work at home, and saved income significantly. This led to a house purchase boom as these sectors of labour looked to change their lifestyles post-Covid.

At the same time, zero interest rates and cheap credit allowed financial institutions to make hay in financial markets and billionaire wealth rocketed as stock and bond markets hit historic highs.

But, for most manual workers in the cities and in low-paid service industries, the pandemic slump was a disaster and with little prospect of returning to “normal” for them in the recovery.

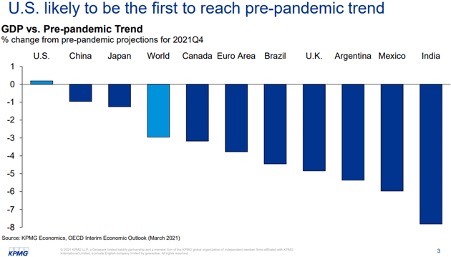

And it’s the advanced capitalist economies and the East Asian states that are recovering best in 2021-22. The so-called global South suffered hugely in the pandemic, with record levels of excess deaths and a massive rise in unemployment and poverty levels. Fiscal support from governments was limited and the rollout of vaccines to get economies going again is way short. Estimates are that the target vaccination levels in these countries will not be achieved until 2023-4!

So, what we are going to see is the major capitalist economies of the West and China returning to pre-pandemic levels of national output by the end of this year or in early 2022, but Latin America, Africa, South Asia failing to do so.

Before the pandemic, the world economy was slowing down. Real GDP growth rates in the G7 were dropping to just 1 percent or lower; the so-called emerging economies had growth rates down to 3 percent (hardly enough to cover increases in population). World trade was declining. Even the giant economies of China and India had slowed.

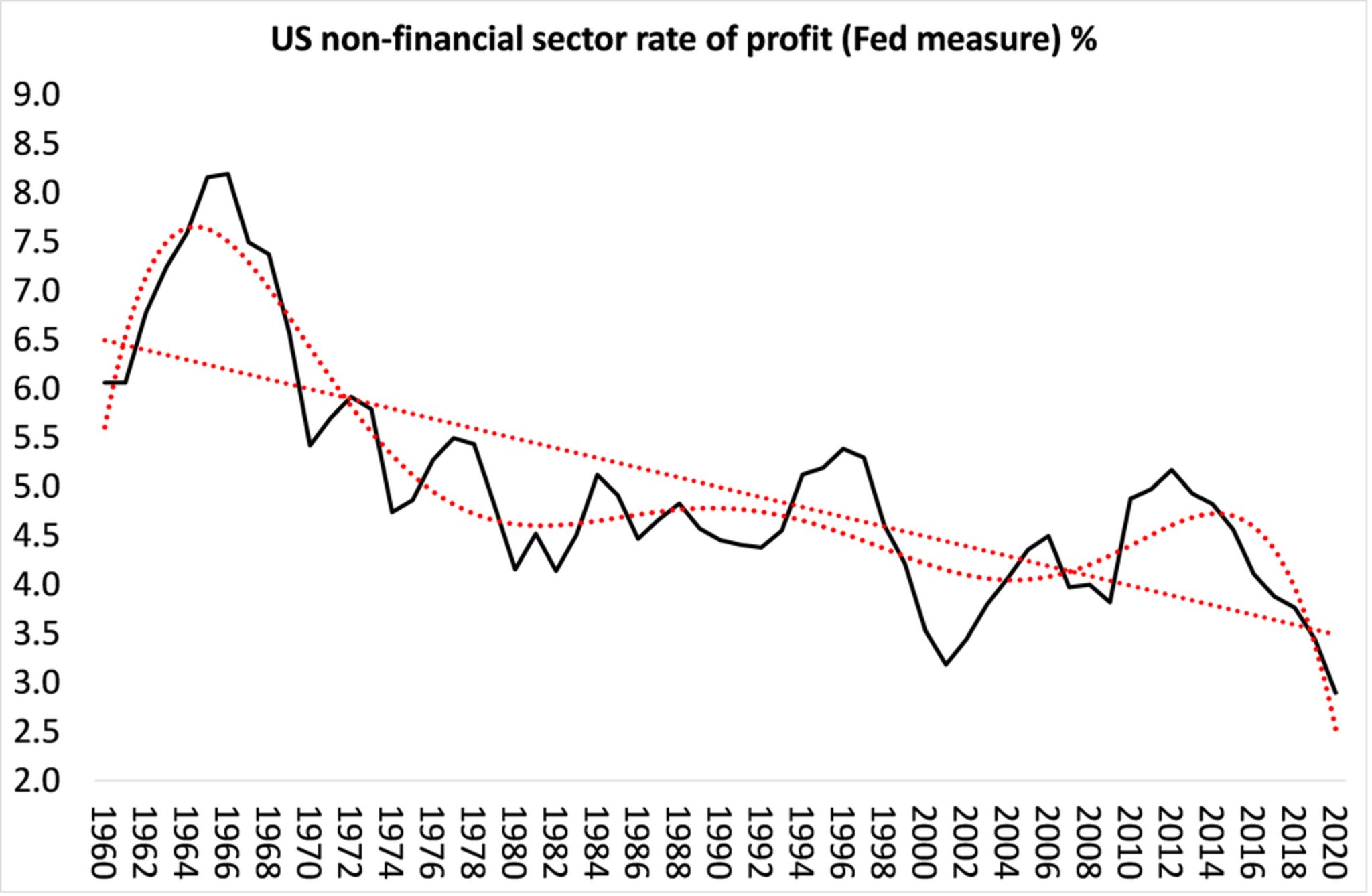

The main reason was that growth in investment in productive assets that can boost the productivity of labor and expand technology and employment had also slowed. In my view, investment and productivity growth are key to developing the productive forces of modern capitalist economies, and they were failing because under capitalism, profitability is the driving force behind investment.

And according to the best estimates, US and global profitability levels are at historic lows. This is the long-term result of the basic contradiction of capitalism: between raising the productivity of labour and sustaining profitability. Over the long term, this cannot be done, and this is the economic Achilles heel of capital.

At first sight, this result seems strange when we read of the huge profits being made by the likes of the so-called FAANGS (the tech and social media monopolies) and Amazon. But these are the exceptions that prove the rule. On average, the profitability of firms in the productive sectors of capitalist economies are low.

That’s partly why profits have been reinvested into financial and other unproductive sectors like property where profitability is higher.

Indeed, it is estimated that before the pandemic, about 15-20 percent of companies in the major economies were what are called “zombies,” i.e., not making enough profit to invest or expand, but just enough to pay wages and service their debts. They are the “living dead” in capitalist terms. At the same time, however, corporate debt is at record highs in most countries, raising the risk of bankruptcies if interest rates were to rise.

All this makes it unlikely that we shall see any significant change post-pandemic from what we saw in the post-great recession decade, i.e., slow growth in investment, low wage growth, poor productivity growth, rising inequality, and unchanged or worsened global poverty.